TaxCycle 15.2.62988.0—T2 and AT1 Certification, T5013/TP-600 Module Rollover

This certified release of TaxCycle T2 and AT1 extends the supported corporate tax year ends up to October 31, 2026. It also rolls over the T5013/TP-600 module to 2026.

To install this version immediately, download the full installer from our website or request a free trial.

Release Highlights

T2 and AT1 Filing Date Extension

TaxCycle supports the preparation and filing of federal T2 and Alberta AT1 corporate tax returns with tax year ends up to October 31, 2026.

T2 File Conversion Message

When opening an in-progress T2 return, TaxCycle may prompt you to convert it to the new module. This message appears if the return’s status is not “Completed” and the corporation’s tax year starts on or after January 1, 2024.

- Click the Convert button or the link to convert the return to the newer module.

- Save the new return. You can choose to delete the old file by answering Yes to the Delete old return question in the dialog box that pops up. Once a file is deleted, it will no longer appear in the Client Manager or in the recent files list.

- The new file extension is .2026T2 and supports returns up to October 31, 2026. To learn more about T2 file name extensions, read the T2 File Name Extensions help topic.

Updated T2 Forms

T2 Corporation Income Tax Return

- Removed checkbox 275 and line 799 for Schedule 65.

Removed line 799 from the T2 Summary.

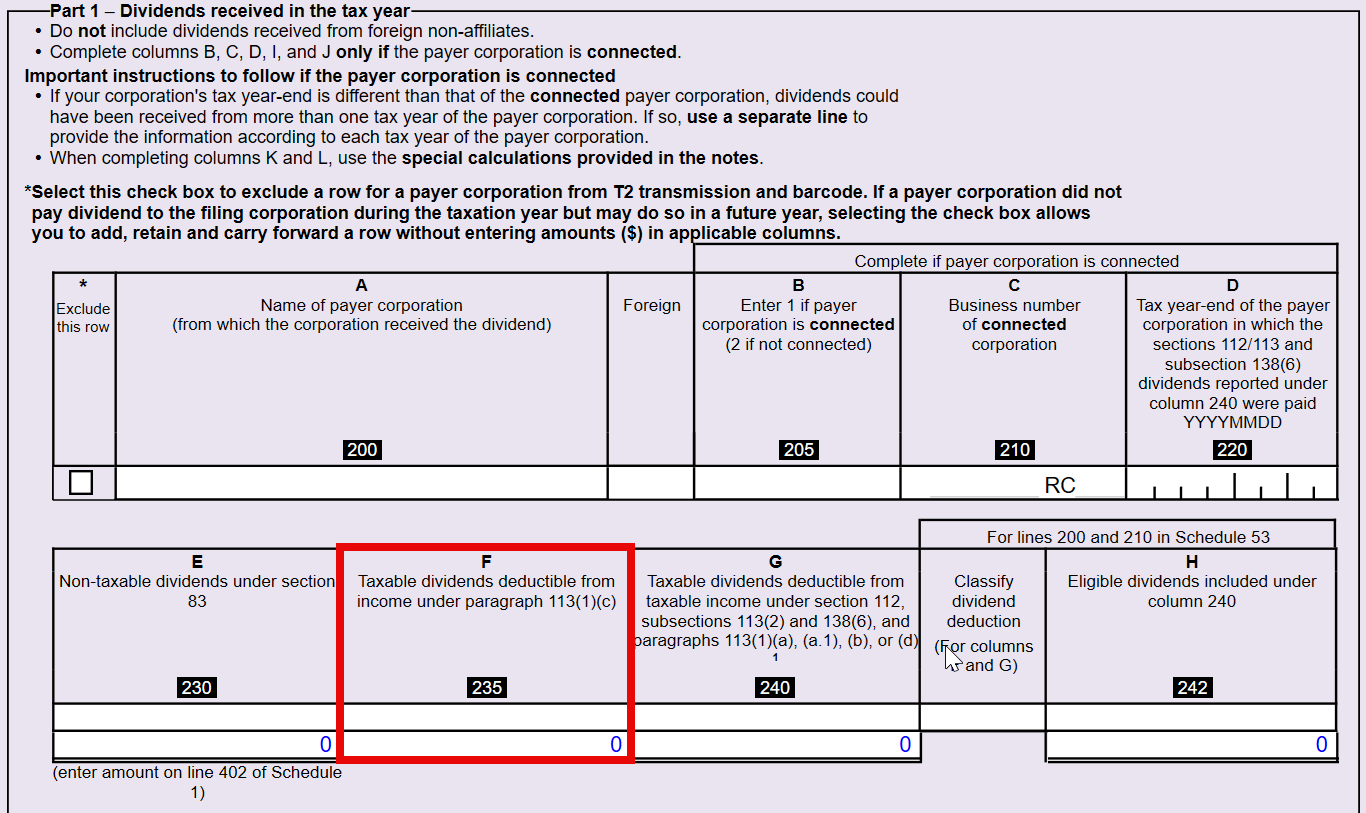

Schedule 3 Dividends Received, Taxable Dividends Paid, and Part IV Tax Calculation

- Added new column 235 to the Part 1 table for taxable dividends deductible from income under paragraph 113(1)(c). Previously, these dividends were entered in an on-screen only field below the Part 1 table.

- When you open an existing file and convert it to the 2026 T2 module, TaxCycle retains the data from the previous fields and moves it to the new column 235.

- Added question 100 to Part 2, which only calculates if you answer “No.”

Schedule 5 Tax Calculation Supplementary

Schedule 8 Capital Cost Allowance (CCA)

TaxCycle version 15.1.61020.0 updated T2 CCA calculations to incorporate the Reaccelerated Investment Incentive Property (RIIP) measures enacted in Bill C-15. At that time, the Canada Revenue Agency (CRA) had not released a revised Schedule 8, so capital cost calculations were adjusted using the old Schedule 8 copy. This release updates Schedule 8 to the latest, official copy incorporating the RIIP measures.

- Part 1: Removed the agreement table and question 105 on immediate expensing and EPOPs.

- Part 2: Added column 226 and removed columns 232, 234, 236, and 238.

Schedule 12 Resource-Related Deductions

- Part 5: Added line 372 reaccelerated Canadian development expenses (RCDE), generally incurred from 2024 to 2034.

- Part 6: Added line 453 for reaccelerated Canadian oil and gas property expenses (RCOGPE), generally incurred from 2024 to 2034.

- The same changes apply to AT1 Schedule 15 and CO-400.

Schedule 21 Federal and Provincial or Territorial Foreign Income Tax Credits and Federal Logging Tax Credit

- Updated to the latest version from the CRA.

- Part 6: Added amount 6E

- Part 7: Added amounts 7F, 7G and 7H

- Part 8: Added amounts 8F, 8G and 8H

Schedule 31 Investment Tax Credit - Corporations

Bill C-15, which received Royal Assent on March 26, 2026, significantly enhanced Canada’s SR&ED programs. We have updated Schedule 31 to reflect these changes.

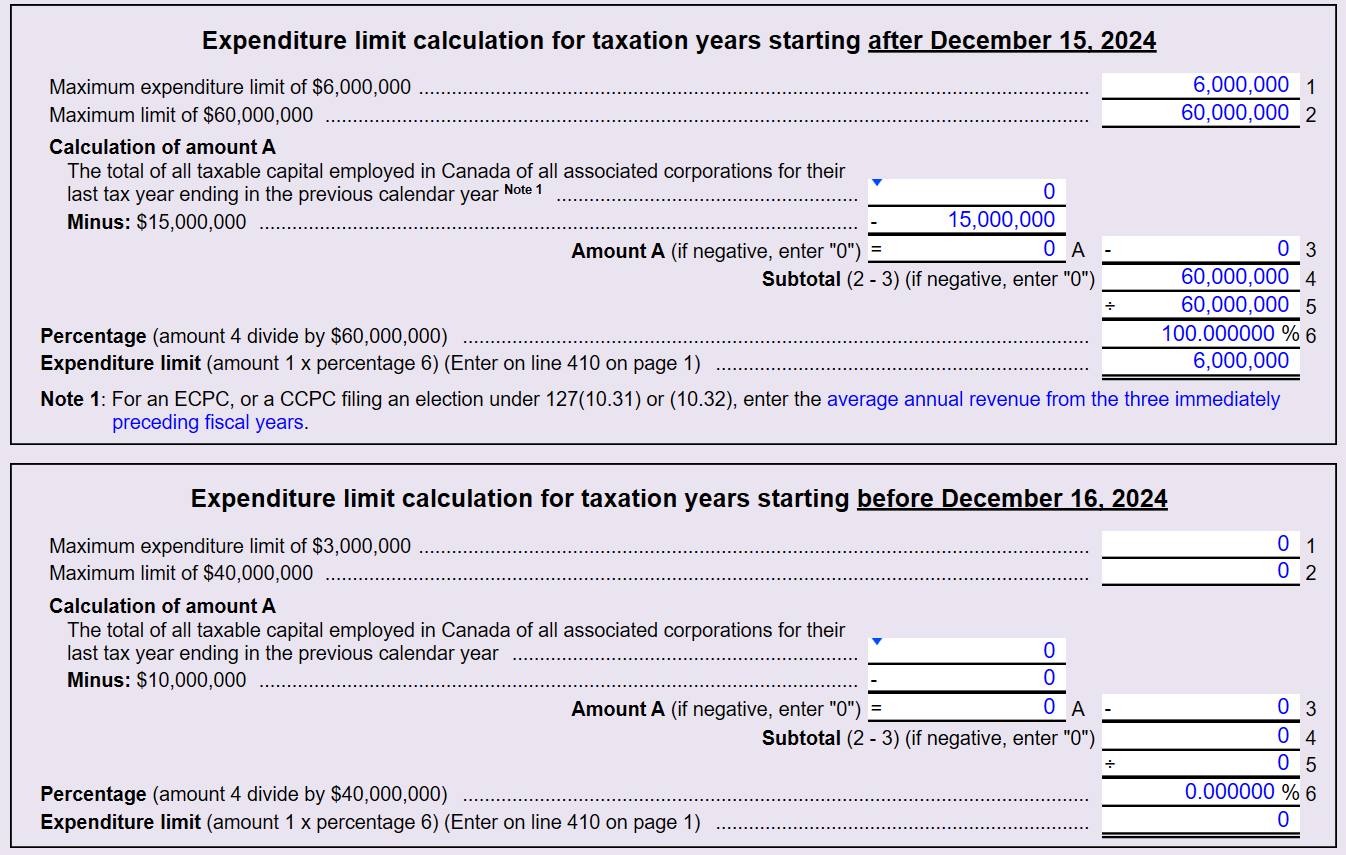

- Qualified SR&ED expenditures now include capital expenditures incurred after December 15, 2024. The annual expenditure limit for taxation years beginning after December 15, 2024, has doubled to $6 million.

- Currently, the expenditure limit begins to decrease when the taxable capital employed in Canada of the Canadian-controlled private corporation (CCPC) and its associated corporations for the previous tax year reaches $10 million and becomes nil starting at $50 million. For a taxation year beginning after December 15, 2024, the expenditure limit begins to decrease when the taxable capital employed in Canada of the CCPC and its associated corporations for the previous tax year reaches $15 million and becomes nil starting at $75 million.

- Access to a 35% refundable investment tax credit (ITC) has been expanded beyond CCPCs. For a taxation year beginning after December 15, 2024, an eligible Canadian public corporation (ECPC) can claim the 35% refundable ITC.

- CCPCs electing under subsection 127(10.31) or (10.32) or ECPCs can use gross revenue instead of taxable capital to calculate the expenditure limit. See Schedule 49 and CGI Worksheet, below.

- Part 8: Added line 360 to record capital expenditures from line 558 of T661.

- Part 9: Added questions 382 (ECPC) and 383 (CCPC electing under 127(10.31) or (10.32)) and line 339.

- Added Part 10B to calculate the enhanced expenditure limit for CCPCs with a tax year starting after December 15, 2024, or an ECPC.

- Part 11: Added lines 440 and 450.

- Part 15: Added fields 15B, 15C, 15D, 15E and 15F.

- Part 23: Added line 185 for the Clean electricity ITC. The corresponding support form is not available at this time.

- Removed Part 23 (Recapture of ITC for corporations and partnerships - childcare spaces) and line 25B (Recaptured childcare spaces ITC) from Part 25.

Schedule 31 Worksheet (S31WS)

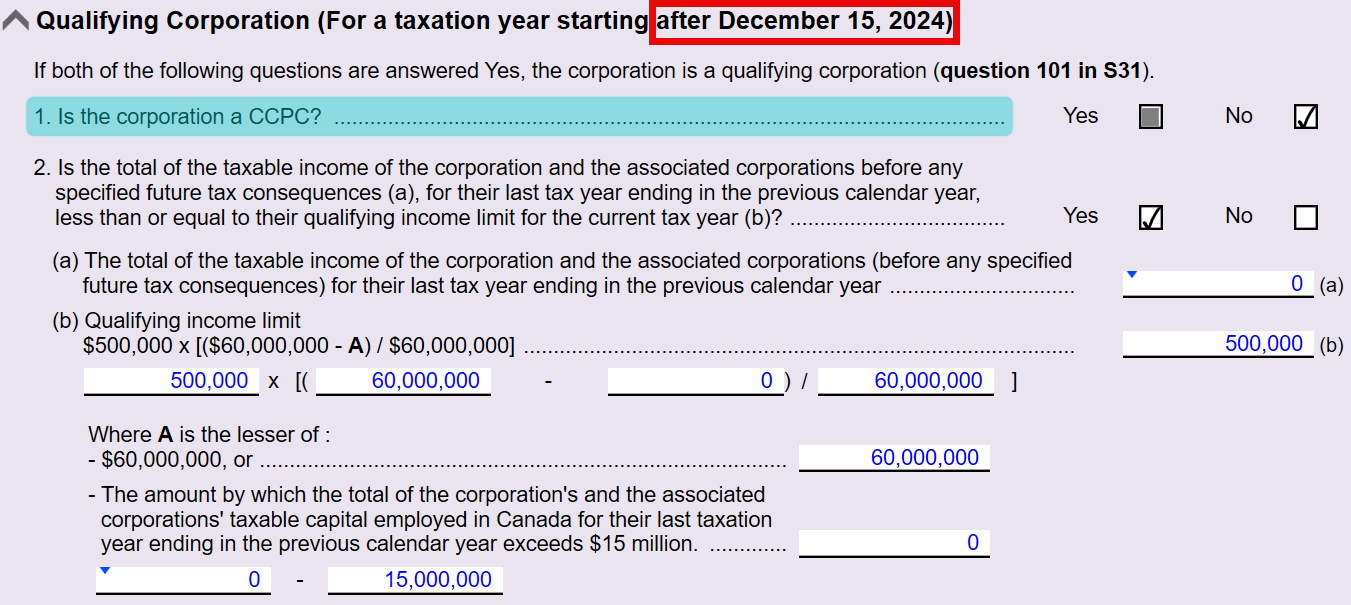

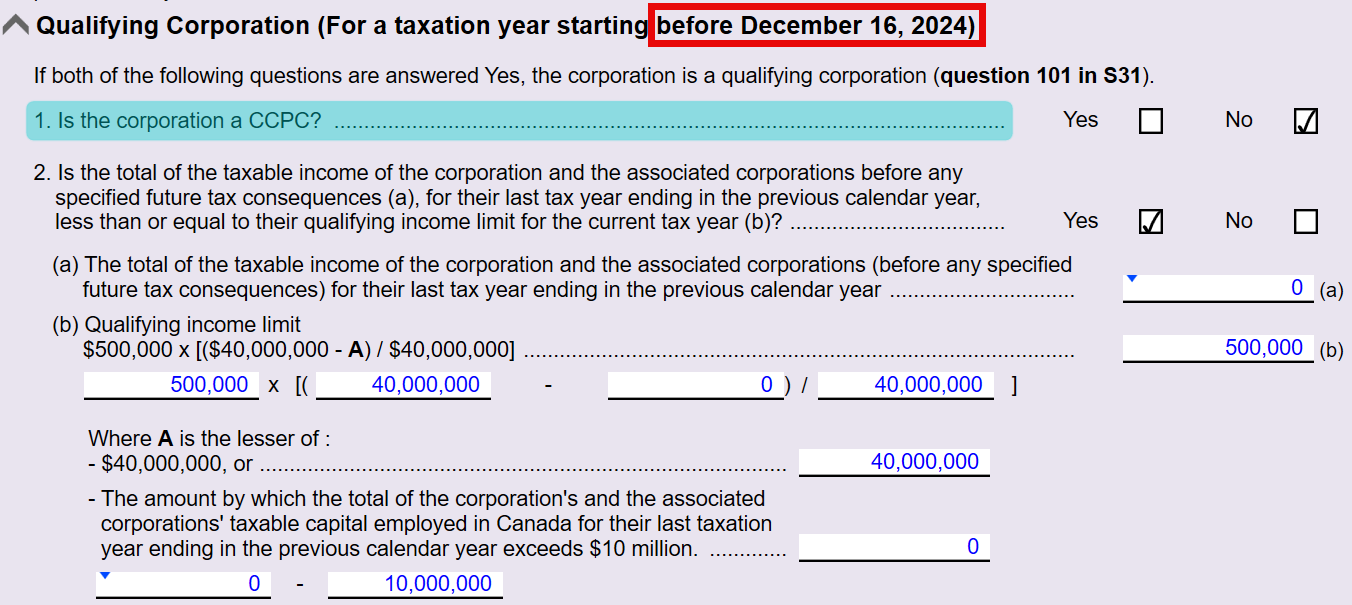

- The definition of a qualifying corporation (ITA subsection 127(2)) has been updated for tax years starting after December 15, 2024, with increased thresholds of $60 million and $15 million.

- For tax years before December 16, 2024, TaxCycle shows the previous support section.

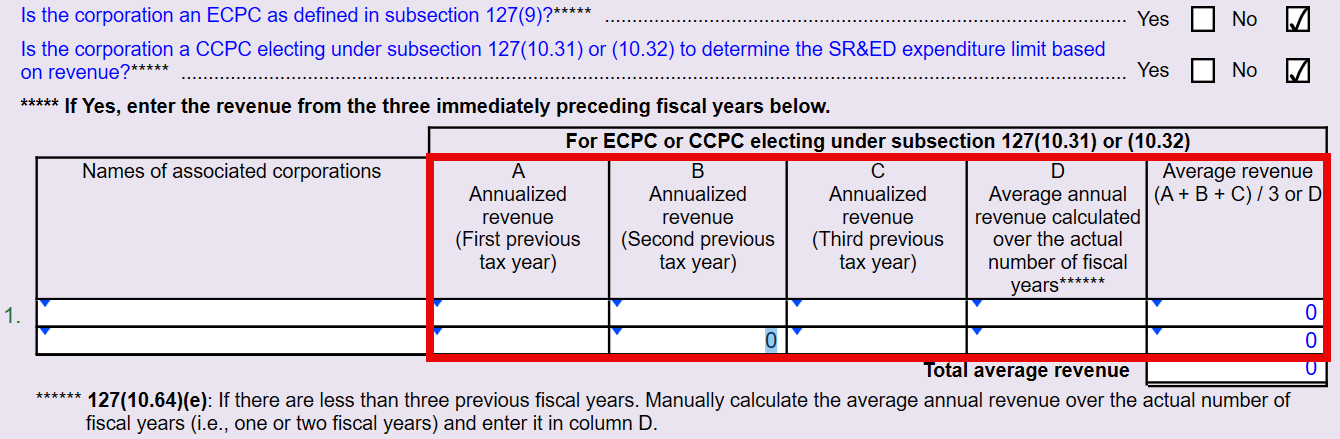

Schedule 49 and CGI Worksheet Agreement Among Associated Canadian-Controlled Private Corporations to Allocate the Expenditure Limit

- Removed line 425.

- For tax years starting after December 15, 2024, the annual expenditure limit doubles to $6 million. Added two on-screen sections to support expenditure limit calculations.

- For an ECPC or CCPC electing under subsection 127(10.31) or (10.32), the expenditure limit is calculated based on the average gross revenue (the average, over the period of three fiscal years immediately preceding and ending before the particular taxation year) instead of taxable capital.

- If this applies, enter the previous years’ annualized revenue (columns A, B and C) in the table, either on S49 or the CGI worksheet.

- If there are less than three fiscal years, the average annual revenue is to be calculated over the actual number of fiscal years (i.e., one or two fiscal years) and enter this amount in column D.

- To allow the allocation of the expenditure limit amongst ECPCs, in the fall of 2026, the CRA will issue a new form (a different type of Schedule 49 for ECPCs). Until this new form is available, you can use the existing Schedule 49 to allocate the expenditure limit among ECPCs. However, the CRA will not administer the allocation until this new form becomes available. We will provide an update as soon as we receive further information from the CRA.

Schedule 65 Air Quality Improvement Tax Credit

- This schedule has been removed.

Schedule 75 Clean Technology Investment Tax Credit

- Part 1: Added column 105.

- Part 2: Added column 212.

- Added Part 5 for amounts allocated from partnerships.

Schedule 76 Clean Technology Manufacturing Investment Tax Credit

- Part 1: Removed column 107 and added column 106.

- Part 2: Added column 206.

- New Part 3 is for amounts allocated from partnerships. Total amounts on lines 350 and 355 flow to line 150 in Part 1 and line 240 in Part 2, respectively.

Schedule 78 Carbon Capture, Utilization, and Storage Investment Tax Credit

- Minor update to version 2202.

- New Part 5 is for amounts allocated from partnerships. Total amounts on lines 550, 555 and 560 flow to line 190 in Part 1, line 325 in Part 3 and line 465 in Part 4, respectively.

T661 Scientific Research and Experimental Development (SR&ED) Expenditures Claim

- Part 1: Removed lines 110 and 125 (fax numbers).

- Added lines and sections:

- Part 1: Lines 106 and 121 for telephone number extensions.

- Part 3: Lines 350, 355, 390 and 400.

- Part 4: 496, 504, 510, 512, 514, 516, 518, 532, 535, 540, 543, 546 and 558 (Capital Expenditures column)

- Part 6A: Column 759 (flows from Schedule 60)

- Added Part 6B and Part 6C.

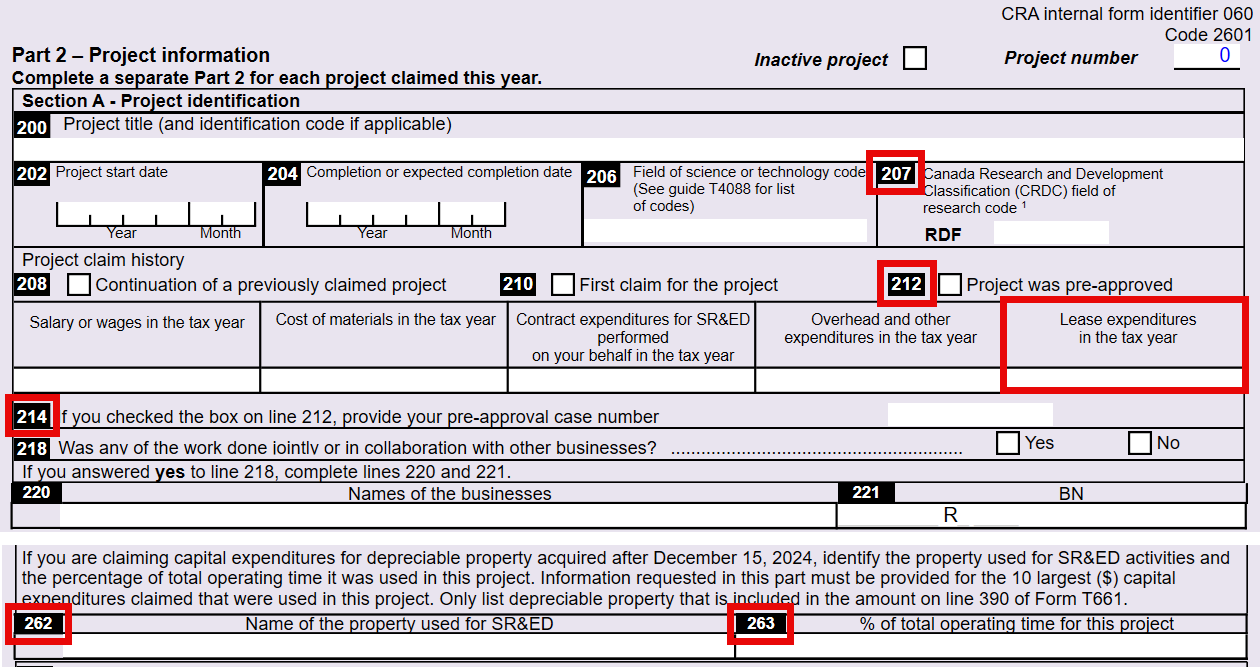

Schedule 60 Scientific Research and Experimental Development (SR&ED) Expenditures Claim Part 2

- Added line 207 for the Canada Research and Development Classification (CRDC) field of research code.

- Added lines 212, 214, 262 and 263, and a lease expenditure field that flows to Part 6 of T661.

T1145 Agreement to Allocate Assistance for SR&ED Between Persons Not Dealing at Arm’s Length

- Added lines 015 and 020 to account for the breakdown between current and capital expenditures.

- Line 010 is now calculated as the sum of lines 015 and 020.

- When you open an existing file in this release, the previous amount from line 010 appears on new line 015.

T1146 Agreement to Transfer Qualified Expenditures Incurred in Respect of SR&ED Contracts Between Persons Not Dealing at Arm’s Length

- Added lines 015 and 020 to account for the breakdown between current and capital expenditures.

- Line 010 is now calculated as the sum of lines 015 and 020.

- When you open an existing file in this release, the previous amount from line 010 appears on new line 015.

Schedule 150 Net Income (loss) for Income Tax Purposes for Life Insurance Companies

Schedule 151 Investment Revenue From Designated Insurance Property for Insurance Companies

- Updated to the latest version.

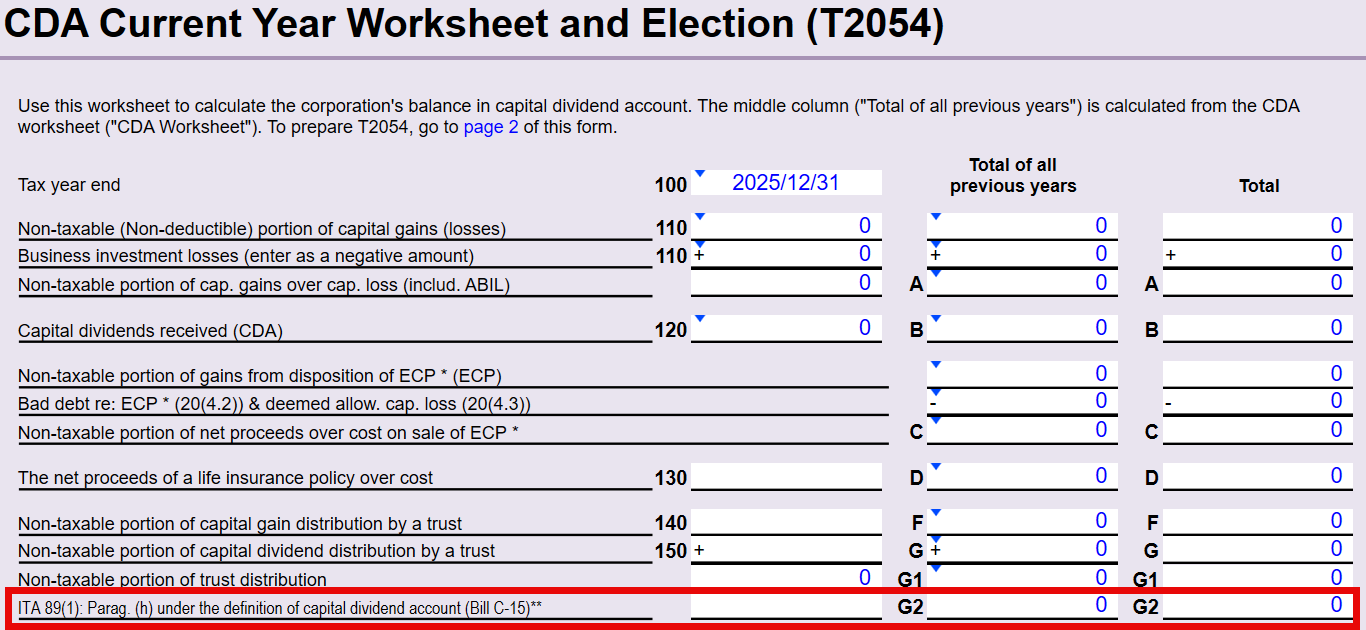

Schedule 89 and T2054 Bill C-15 paragraph 89(1)(h)

- Added a new row of fields to the T2054 Prior Year, Current Year and Next Year worksheets to account for the CDA addition under new ITA paragraph 89(1)(h) as enacted in Bill C-15. If the new ITA paragraph 89(1)(h) applies, enter the amount in the applicable fields.

- As of this release, the CRA is working on updated Schedule 89 to incorporate the above fields; however, there is no clear date on when the updated S89 will become available. In the meantime, the CRA has asked that the CDA addition under ITA 89(1)(h) be included in Part 2A column 5 or Part 2B column 4 of Schedule 89. In addition, the CRA has requested that a letter be attached to S89 explaining that the CDA addition under ITA 89(1)(h) has been included in Schedule 89 Part 2A column 5 and/or Part 2B column 4.

TX-19 Asking for a Clearance Certificate

- Updated to the latest version.

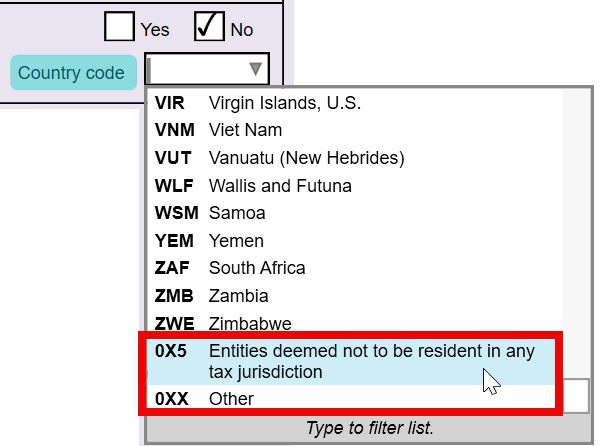

T106 Summary Form (T106S)

- Added country codes 0X5 and 0XX to the question 9 dropdown list.

Schedule 307 Newfoundland and Labrador Corporation Tax Calculation

- Revised to reflect Newfoundland and Labrador’s Bill 16, which received Royal Assent on June 2, 2026, and which reduces the small business income tax rate by 0.5% (down to 2%) for days in 2026.

Schedule 500 Ontario Corporation Tax Calculation

- Updated the calculation to reflect Ontario’s Bill 97, which reduces the small business income tax rate from 3.2% to 2.2%, effective July 1, 2026.

Schedule 572 Ontario Made Manufacturing Investment Tax Credit

- Added Part 4 and Part 6 for the non-refundable portion of the tax credit.

- Line 460 in Part 4 flows to line 421 of Schedule 5.

T666 British Columbia (BC) Scientific Research and Experimental Development Tax Credit

- Updated to reflect BC’s Bill 2, which received Royal Assent on April 16, 2026:

- Expanded SR&ED eligibility to include ECPCs, as introduced in federal Bill C-15.

- Doubled the BC expenditure limit to $6 million for taxation years starting on or after December 16, 2024, as announced in federal Bill C-15.

Updates to Other Provincial and Territorial SR&ED Forms

We have revised the calculations for the provincial SR&ED forms below to take into account the SR&ED measures enacted in Bill C-15. Specifically, capital expenditures as well as expenditures on shared-used equipment are now included in the calculation of qualified expenditure.

- Schedule 301 (Newfoundland and Labrador)

- Schedule 340 (Nova Scotia)

- Schedule 360 (New Brunswick Research and Development Tax Credit)

- Schedule 380 (Manitoba)

- Schedule 508 and S580WS (Ontario)

- Schedule 403 (Saskatchewan) - expenditure limit doubles to $2 million.

Alberta AT1 Form Changes

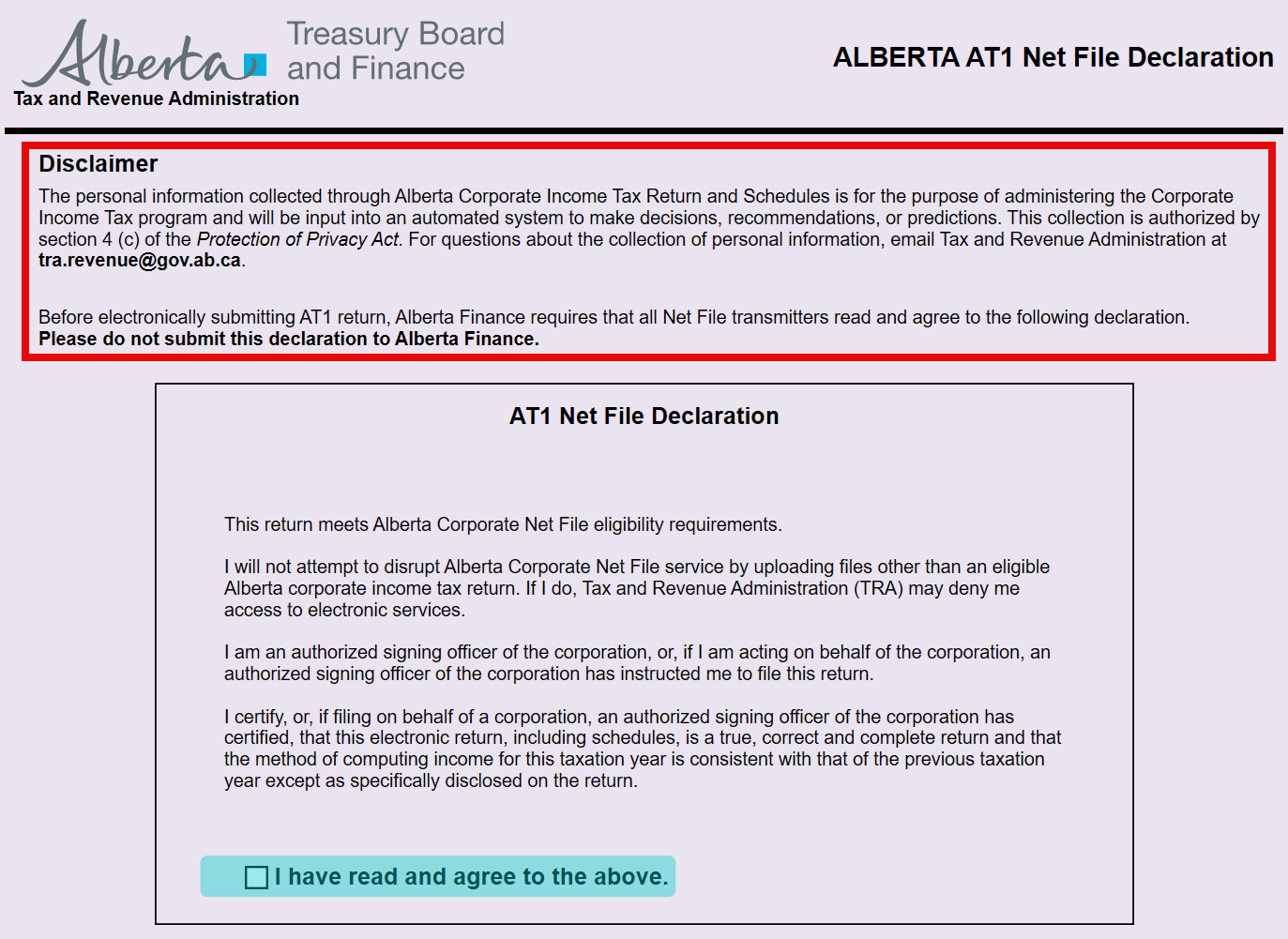

AT1 Net File Declaration

- Added a disclaimer to the top of the AT1 form. Agreeing to the net file declaration confirms you have read and understood the disclaimer.

AT1 Schedule 12 Alberta Income/Loss Reconciliation

Updated to assign official line numbers to the following fields, now included in the AT1 NetFile transmission and AT1 Return and Schedule Information (RSI):

- Line 130 - Restricted interest and financing expenses (Alberta)

- Line 131 - Restricted interest and financing expenses (federal)

- Line 140 - Employer deduction in respect of non-qualified securities (Alberta)

- Line 141 - Employer deduction in respect of non-qualified securities (Alberta)

AT1 Schedule 15 Alberta Resource Related Deductions

AT1 Schedule 21 Alberta Calculation of Current Year Loss and Continuity of Losses

- Added line numbers to 002 and 012.

- Added a section to calculate Restricted interest and financing expenses (RIFE).

Minor Updates

The following forms received minor updates:

- AT4930 Alberta Consent

- AT1 Schedule 4 Alberta Foreign Investment Income Tax Credit

- AT1 Schedule 16 Alberta Scientific Research Expenditures

CO-17 Form Changes

CO-1029.8.36.PS Tax Credit to Support Print Media Companies

The 2026 Québec budget increased the annual limit on line 15 from $75,000 to $85,000 for taxation years ending after March 18, 2026. However, if the corporation’s taxation year ends after March 18, 2026, and the corporation has made a written election to Investissement Québec to exclude the tax credit amendments in the 2026–2027 budget from applying, the annual limit continues to be $75,000.

In this case, you can check the box at the bottom of the form to continue to apply the $75,000 limit. This update has been approved by Revenu Québec.

CO-400 Resource Deduction

- Adjusted the calculations in Parts 3.1 and 4 to incorporate reaccelerated COGPE and reaccelerated CDE as introduced in federal Bill C-15. Approved by Revenu Québec.

RD-222 Deduction Respecting Scientific Research and Experimental Development Expenditures

Adjusted to incorporate changes made to T661. Revised the calculations of the following lines of RD-222:

- Line 35 (column A): flows from T661 line 350 when method A is selected.

- Line 35 (column B): flows from T661 line 350 when method B is selected.

- Line 37 (column B): flows from T661 line 355 when method B is selected.

- Line 47 (column B): T661 line 390 does not break out office equipment or furniture separately. Enter this amount manually.

- Line 48 (column B): Flows from T661 line 390 minus the amount entered in line 47 (column B) when method A is selected. Line 48 (column B) flows from T661 line 390 when method B is selected.

T2 Planning and Training Files

This release allows you to create a T2 file and mark it for planning or training purposes after you carry forward a prior-year T2 tax return. See the Planning and Training Files help topic to learn more.

T3 File Conversion Message

When opening an in-progress T3 return, TaxCycle may prompt you to convert it to the new module.

- Click the Convert button or the link to convert the return to the newer module.

- The new file extension is .2026T3. Save the new return. You can choose to delete the old file by answering Yes to the Delete old return question in the dialog box that pops up. Once a file is deleted, it will no longer appear in the Client Manager or in the recent files list.

Rollover of T5013/TP-600 to 2026

The new module for TaxCycle T5013 allows you to begin data entry for 2026 federal and Québec partnership returns. Please note the following:

- You can carry forward 2025 T5013 returns from TaxCycle and competitors, including the creation of stub period returns.

- You can use this module to file partnership returns with fiscal year ends in 2026.

- The government forms are the 2025 forms updated to include 2026 indexed amounts and budget changes announced or estimated based on the information we have at this time. A review message appears on the year-end date field and in a bulletin at the top of the forms to remind you of this.

- This module permits CRA Internet File Transfer (XML) and transmission of RL slips to Revenu Québec.

- The T1135 and T1134 in this module are certified for filing for year ends on or before October 31, 2026.

New and Updated Forms

- Added form TP-1079.8.BE (Foreign Property Return). This form is the Québec equivalent of the T1135 and must be paper filed, when applicable, with the TP-600.

- Added new fields on the T5013Partner worksheet to allow adjustments to carrying charges for limited partners where ARA rules limit the amount that can be allocated in the year. Limited amounts are added to the limited losses available to carry forward at year end. For more information, refer to the CRA’s T4068, Guide for the Partnership Information Return (T5013 Forms), Box 210.

- Removed the question about blank Schedule 130 from the Info worksheet since it is no longer required.

We have updated the following forms to the latest version:

- GST191 and GST191WS New Housing Rebate Application for Owner-Built Houses

- RC7191-ON Ontario Rebate Schedule

- T1261 Application for a Canada Revenue Agency Individual Tax Number (ITN) for Non-Residents

Customer Requests

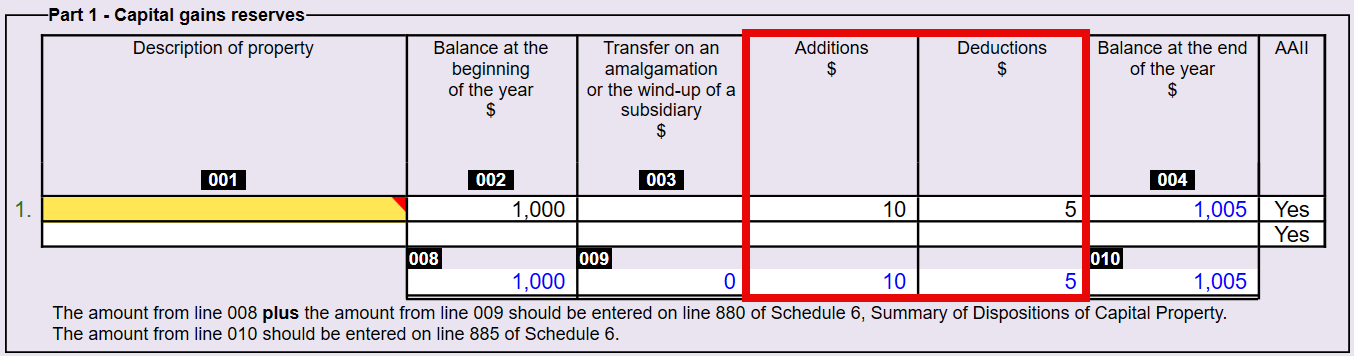

- T2—Improved forms S13, S13WS, AS17 and QC13 by splitting the “additions or deductions” column into two separate columns.

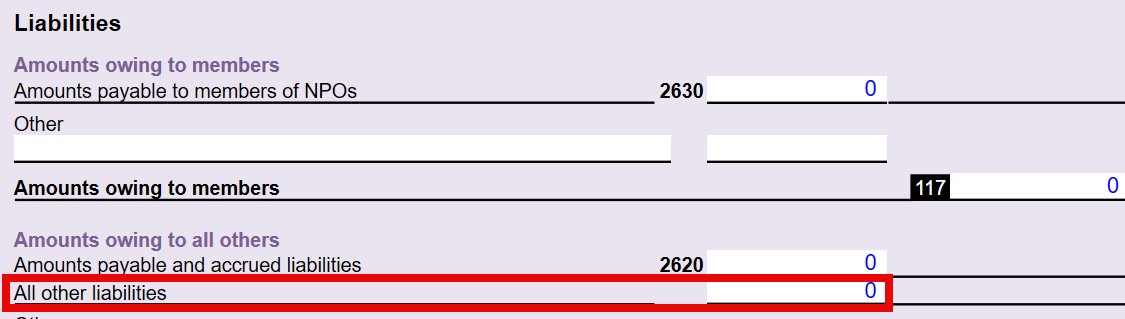

- T2—Added a new field for “all other liabilities” on T1044WS to calculate remaining liabilities from S100 and ensure the total liabilities amount aligns on both forms.

- T2—Improved the Info worksheet by removing the subsidiary wind-up table. TaxCycle now calculates lines 42a and 42b of CO-17 directly from CO-17.S.36 (QC24).

Resolved Issues

- Known Issue: CO-17S.3 (QC3) Part 2 Table Not Populating Correctly from Schedule 3

- Customer Reported T5013—Fixed an issue where selecting to transmit documents before electronically filing the T1135 or T1134 was blocking transmission of the form. TaxCycle now only shows the review messages on the T1135 or T1134 FRRMS Submit e-Documents transmission.

- Customer Reported T5013—Improved e-signature stability when printing multiple print sets simultaneously. This initial update reduces occurrences while a more robust solution is finalized in an upcoming release.