Immediate Expensing of CCA (T1)

This topic covers immediate expensing for personal tax returns, in TaxCycle T1. To learn how to apply the measure to corporate or partnership returns, see T2 and T5013 Immediate Expensing of CCA.

General Rule

The Department of Finance has introduced a temporary tax incentive measure called “immediate expensing incentive.” This incentive allows an eligible person or partnership (EPOP) to immediately expense costs of certain depreciable capital property (known as “immediate expensing property”) in the year of acquisition up to an annual maximum limit of $1.5 million. This annual limit is called the immediate expensing limit and it must be shared with any associated EPOPs. This limit is subject to proration if a tax/fiscal year of an EPOP is less than 51 weeks.

Abbreviations and Definitions

The following abbreviations are used throughout this topic.

- EPOP Eligible Person or Partnership (entity eligible to claim immediate expensing)

- IEL Immediate Expensing Limit ($1.5 million limit)

- IEP Immediate Expensing Property (eligible property)

- DIEP Designated Immediate Expensing Property (elected/designated eligible property)

An EPOP is defined as:

(a) a corporation that was a Canadian-controlled private corporations (CCPC) throughout the year;

(b) an individual (other than a trust) who was resident in Canada throughout the year; or

(c) a Canadian partnership, all of the members of which were, throughout the period, persons described in paragraphs (a) or (b).

IEP refers to eligible capital asset additions and is defined as property of a prescribed class other than property included in any of Classes 1 to 6, 14.1, 17, 47, 49 and 51. If the EPOP is

- A CCPC, the IEP is the capital assets acquired after April 18, 2021, and before 2024.

- An individual or a Canadian partnership all the members of which are individuals throughout the taxation/fiscal year, the IEP is the capital assets acquired after December 31, 2021, and before 2025.

- A Canadian partnership, all of the members of which are not individuals throughout the fiscal year, the IEP is the capital assets acquired after December 31, 2021, and before 2024.

In order to apply the immediate expensing incentive, an EPOP must “designate” IEP as DIEP (“designated immediate expensing property”). This designation occurs automatically through preparing a CCA schedule for any business (T2125), fishing (T2121), farming (T2042), AgriStability/AgriInvest (T1163/T1273) or rental (T776) statement.

In accordance with the definition of an EPOP, above, for the purposes of sharing the immediate expensing limit among associated EPOPs, you must complete an associated table in Area G of the CCA worksheet for the statement. TaxCycle will automatically complete this table based on the data in the IEL table (discussed in more detail later).

An individual’s business, fishing, farming or rental operation with a capital cost of IEP that exceeds $1.5 million in a taxation year, and that has immediate expensing property ordinarily included in more than one CCA class, can decide which CCA class to attribute the immediate expensing incentive. Any remaining UCC may be subject to additional capital cost allowance deductions under the existing CCA rules (AIIP).

The amount of immediate expensing deduction allowed to be deducted is equal to the lesser of:

(a) the EPOP’s immediate expensing limit for the taxation year (all or portion of the $1.5 million limit);

(b) the UCC to the EPOP as of the end of the taxation year (before making immediate expensing deduction) of property that is DIEP for the taxation year, and

(c) if the EPOP is not a CCPC (that is an individual other than a trust), the amount of income, if any, earned from the source of income that is a business or property (computed without regard to paragraph 20(1)(a) of the Act) in which the relevant DIEP is used for the eligible person or partnership’s taxation year.

VERY IMPORTANT! Point (c), above, applies only to individuals (T1) and partnerships (T5013). Eligible individuals and partnerships cannot claim immediate expensing deduction to create or increase a loss before claiming any other CCA (see example below).

For example, if an individual carries on a self-employment business which has $10,000 of net income before CCA, recapture and terminal loss, the maximum amount of immediate expensing amount cannot exceed $10,000.

Example

For example, an EPOP (individual taxpayer) invests $3,000,000 in equal amounts to acquire the following three properties:

- Class 7 (15%): $1,000,000

- Class 10 (30%): $1,000,000

- Class 50 (55%): $1,000,000

Although the taxpayer could designate any of the three properties as DIEP, it is expected that it would generally designate, for purposes of the immediate expensing incentive, starting with property that falls under CCA classes that would otherwise offer the lowest CCA deduction. By doing so, the EPOP would be able to maximize its CCA claim. Simply put, the CCA claim is maximized if the immediate expensing incentive is applied to class 7, class 10, and then class 50—in this order—as illustrated below.

| CCA Class (rate) |

Cost of

Acquisitions |

Immediate

Expensing |

1st year Allowance

on Remainder of Class |

Total First-Year

Allowance |

| Class 7 (15%) |

$1,000,000 |

$1,000,000 |

$0 |

$1,000,000 |

| Class 10 (30%) |

$1,000,000 |

$500,000 |

$225,000 |

$725,000 |

| Class 50 (55%) |

$1,000,000 |

$0 |

$825,000 |

$825,000 |

| Total |

$3,000,000 |

$1,500,000 |

$1,050,000 |

$2,550,000 |

Enable Automatic Calculations

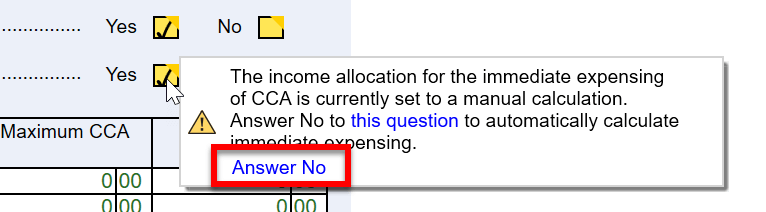

TaxCycle offers two ways of calculating the immediate expensing incentive, depending on how you answer the following questions on the CCAClaim worksheet. You can choose to:

- Manually allocate the immediate expensing limit to each DIEP.

- Manually allocate the income earned from the business or property in which DIEP is used.

The default for both questions in TaxCycle T1 2022 is Yes, manually allocate the immediate expensing limit and the income earned whether you create a new file or open an existing file. This protects the calculations and CCA claims during the middle of personal tax filing season.

To activate the automatic calculation, answer No to these two questions. You must do this on each income statement in the file. TaxCycle will automatically calculate the immediate expensing claim as you enter capital asset additions on the Asset Manager or the CCA worksheet. TaxCycle will remind you to do this in a review message and you can use the Quick Fix solution to automate the claim.

In the 2023 T1 module, we will set the default to No for these questions, similar to the implementation in T2/T5013.

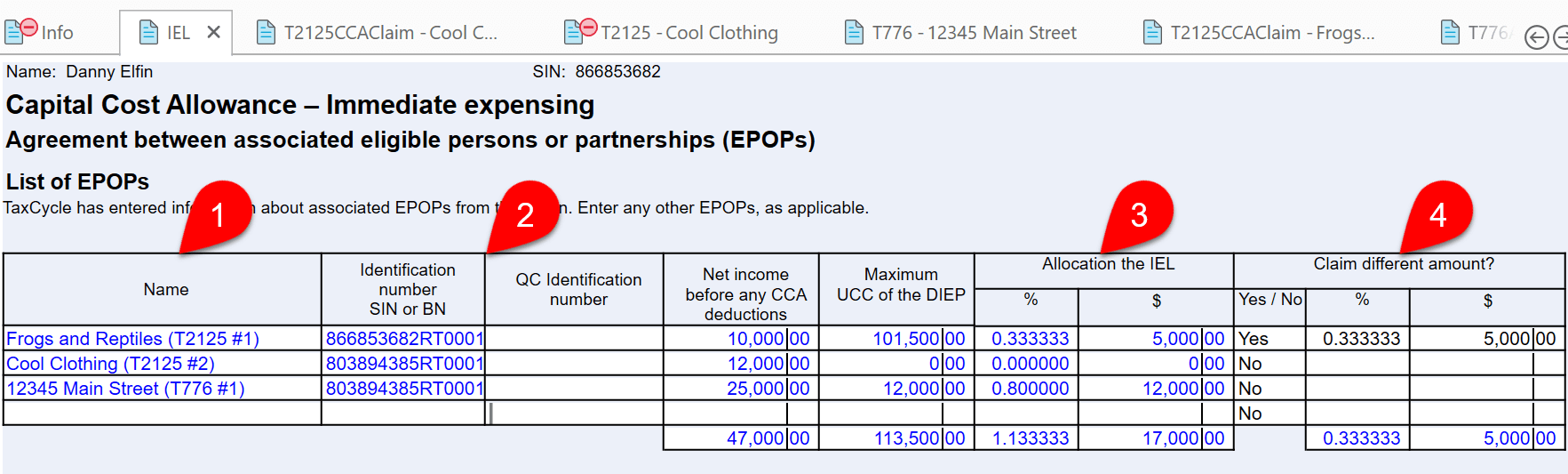

Immediate Expensing Limit (IEL) Worksheet

Individual taxpayers must share the $1.5 million immediate expensing limit between EPOPs. To support the allocation of this limit, TaxCycle T1 contains the Immediate Expensing Limit (IEL) worksheet.

- TaxCycle automatically completes a row on each worksheet for each income statement (T776, T2125, etc.) in the return. The worksheet will also show any income statements shared with a spouse or partner in the same file.

- The social insurance number, business number and Québec identification number flow from the related income statement to this form.

- Based on the answer to the questions on each CCA Claim worksheet, above, TaxCycle will automatically calculate and allocate the IEL. Remember, eligible individuals cannot claim an immediate expensing deduction to create or increase a loss. TaxCycle takes this into account when calculating the allocation.

- If you would like to allocate a different IEL manually, select Yes and enter either the percentage or amount.

Asset Manager and CCA Worksheet

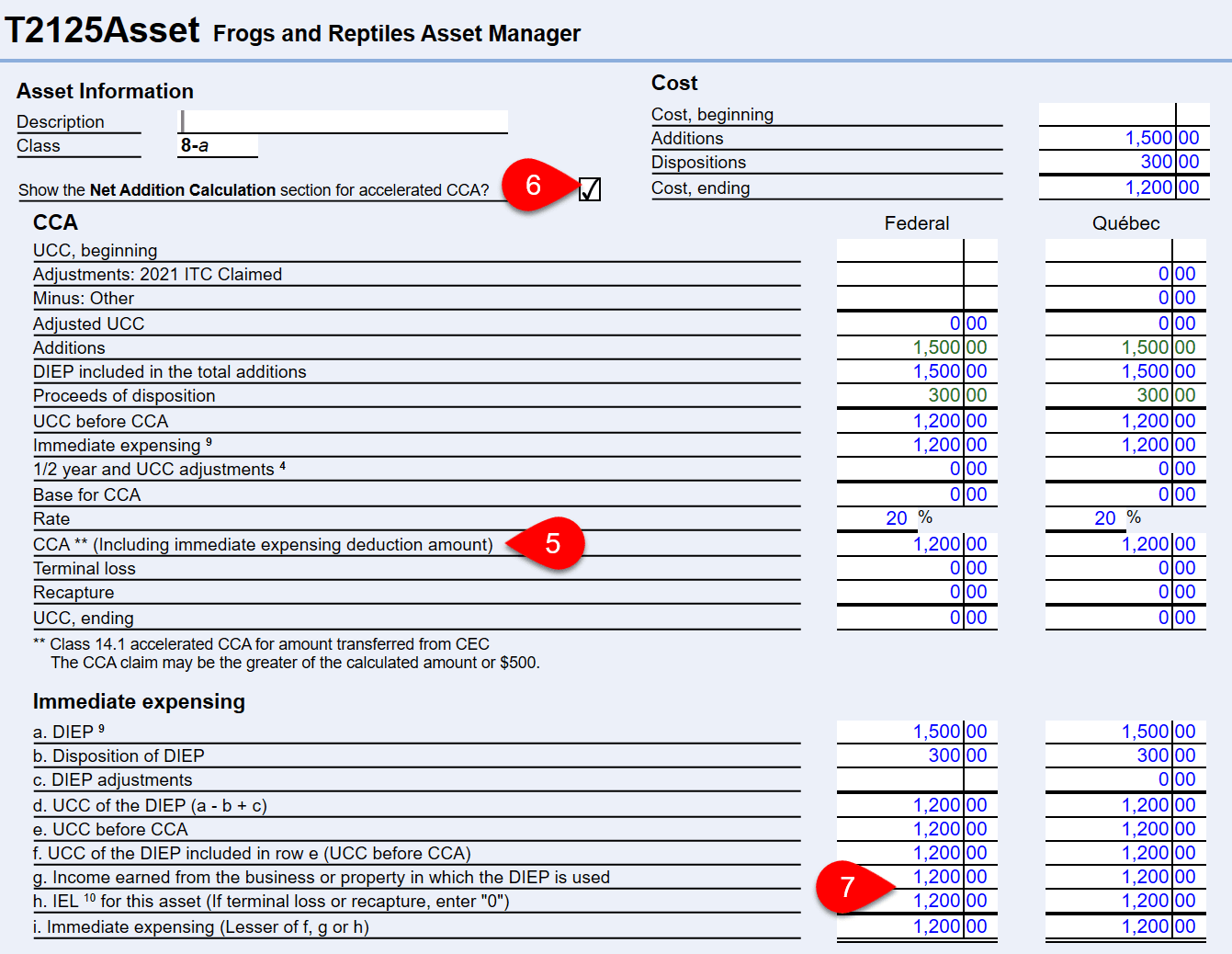

The Asset Manager contains a section to calculate the immediate expensing deduction:

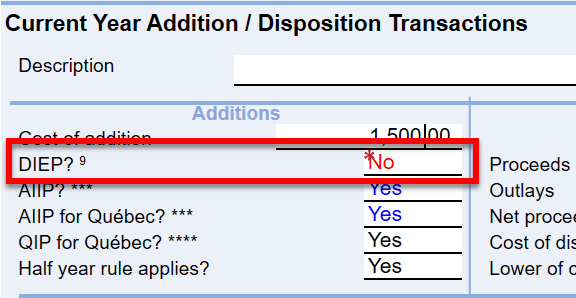

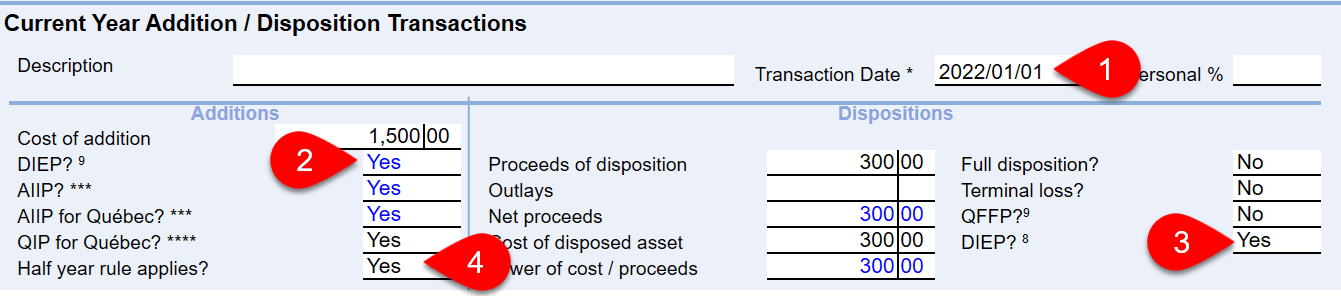

- To claim immediate expensing for an addition, enter the transaction date.

- If the transaction date falls after 2021, and before 2025, TaxCycle will automatically answer Yes to the DIEP? question, making the addition eligible for the immediate expensing deduction.

- For a DIEP acquired and disposed of in the same tax year, enter the details of the disposition and answer Yes to the DIEP? question in the Dispositions column on the right side of the same section.

- IMPORTANT! Generally, the half-year rule is suspended for an eligible addition. This occurs automatically in TaxCycle when calculating immediate expensing. DO NOT answer NO to the half-year rule question on the asset manager to achieve this result. Answer the question based on whether the half-year rule would apply in normal circumstances and TaxCycle will take care of the rest.

- If, after entering the addition, the EPOP is eligible to claim the immediate expensing deduction, TaxCycle will automatically calculate the immediate expensing deduction and include it in the total CCA claim field further up the form.

- To see the full calculations, check the box at the top of the page to show the Net Addition Calculation. This expands the form to display the Immediate expensing section and display the calculated income earned and IEL.

- To change the amounts on lines g and h on the Asset Manager for each income statement, do not override them. First, return to the CCA Claim worksheet and change your answers to the manual allocation questions there. Lines g and h will become editable fields so you can tweak the distribution between various assets.

- The table on the CCA worksheet also contains additional columns to accommodate the immediate expensing calculation.

Québec Forms

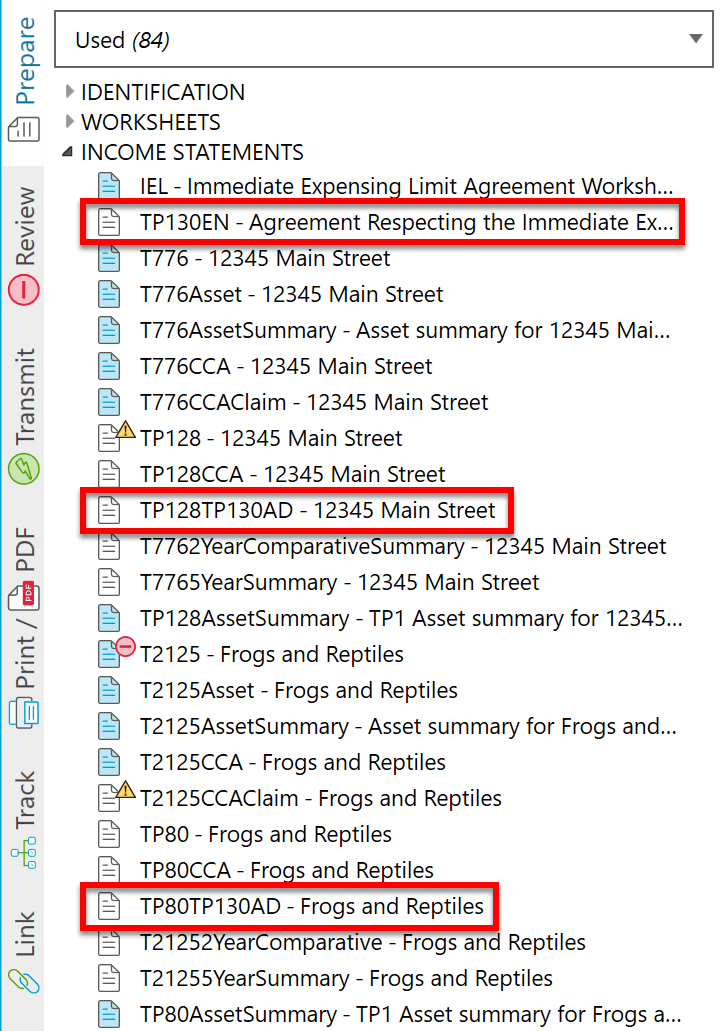

Québec has separate forms to calculate, allocate and claim immediate expensing. They are forms TP-130.AD and TP-130.EN.

- Form TP-130.EN serves the same purpose as the IEL worksheet. Like the IEL worksheet, there is one form for all income statements.

- Form TP-130.AD appears automatically as part of each income statement form set when applicable, along with the Québec equivalent income statement. For example, the equivalent Québec form to the T2125 is the TP-80. The related TP-130.AD form in TaxCycle has the name TP80TP130AD in the Prepare sidebar or when you search for it in F4 Fast Find.

Disabling Immediate Expensing Calculations

If you do not wish to apply immediate expensing to an income statement, go to the CCAClaim worksheet and override the answer to the question about applying the calculations.

You must do this separately for each income statement.

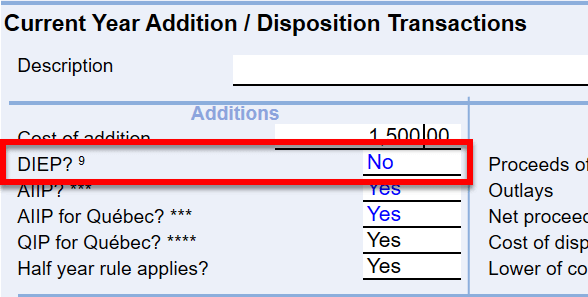

Once you override this question, additions entered on the Asset Manager will no longer show as eligible for immediate expensing.

To exclude a specific addition from immediate expensing, do not override the question on the CCAClaim worksheet. Instead, override the answer to the DIEP question on the Asset Manager to No. The addition will still qualify for Accelerated CCA (AIIP).