T2 Optimizations

The Optimizations worksheet in TaxCycle T2 allows you to control optimizations in corporate tax returns, determine whether to optimize for minimizing or maximizing taxable income, or to turn off optimizations altogether.

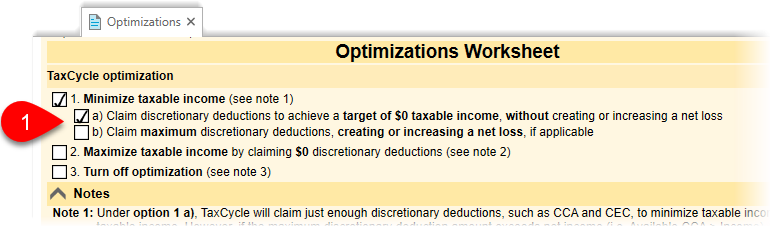

Optimization Goal

The Optimizations worksheet allows you to see and customize optimizations for the taxpayer.

- At the top of the worksheet, select the optimization goal, or disable the optimizations by checking the box to Turn off optimization.

- You can set a default for this worksheet in New File options. Learn how in the New File Options help topic.

- Further down the worksheet, you can see and adjust individual optimizations for federal and provincial deductions.

Order of Calculations

When optimizations are enabled, TaxCycle applies the deductions in the following order:

- Starting with deductions on Schedule 1 to arrive at net income (T2 jacket, line 300, page 3):

- Capital cost allowance (CCA) from Schedule 8

- Cumulative eligible capital (CEC) deduction from Schedule 10

- SR&ED deductions from T661

- Resource deductions from Schedule 12

- Claiming the deductions to arrive at the taxable income (T2 jacket, line 360, page 3):

- Donations from Schedule 2

- Losses from Schedule 4

Example

Read the following scenario for an explanation of the various optimization goals.

| Name of corporation |

Company XYZ |

| Net income from S125 |

$12,000 |

| Class 1, opening UCC |

$987,986 |

Maximum available annual CCA

($987,986 × 4%) |

$39,519 |

Options 1a, 1b and 2

The results of each optimization goal are:

- Option 1a—Claim just enough CCA to offset the taxable income to zero.

- Option 1b—Claim the full annual available CCA of $39,519 to create a non-capital loss.

- Option 2—Claim zero CAA to maximize taxable income (a looming future loss will be carried back to the previous tax years).

TaxCycle applies the deductions in the following order:

- Starting with deductions on Schedule 1 to arrive at net income (T2 jacket, line 300, page 3):

- Capital cost allowance (CCA) from Schedule 8

- Cumulative eligible capital (CEC) deduction from Schedule 10

- SR&ED deductions from T661

- Resource deductions from Schedule 12

- Claiming the deductions to arrive at the taxable income (T2 jacket, line 360, page 3):

- Donations from Schedule 2

- Losses from Schedule 4

Option 3

The last option consists of first claiming the T2 jacket deductions, such as donations and non-capital losses, before claiming Schedule 1 deductions, such as CCA and CEC.

This option may be useful, for example, if a non-capital loss or donation is going to expire soon and you prefer to use it first and preserve as much CCA and CEC claim for the following year.

For an explanation of this option, let’s look at Company XYZ with some variations:

| Name of corporation |

Company XYZ |

| Net income from S125 |

$12,000 |

| Class 1, opening UCC |

$500,000 |

Maximum available annual CCA

($500,000 × 4%) |

$20,000 |

| Non-capital loss due to expire soon |

$11,000 |

By choosing to claim the non-capital loss first before CCA, TaxCycle will preserve as much future CCA as it can.

To select this, choose Option 1 WITHOUT selecting sub-option a or b.